Flood Insurance to fit your budget and needs

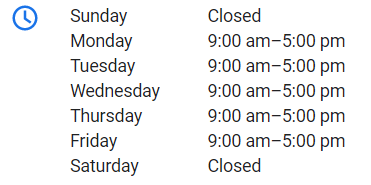

Low Cost Flood Insurance in Savannah

Do I Need Flood Insurance?

Many conditions can cause flooding: spring thaws, heavy rains, hurricanes and the rapid accumulation of rain after a wildfire are just some of them. And, while certain areas are prone to flooding, it can happen anywhere and at any time. According to Fema.gov, floods are the No. 1 natural disaster in the United States. "All it takes is a few inches of water to cause major damage to your home and its contents," the federal government-run website declares. So, are you prepared? Beyond readying your home and developing a family emergency plan, being prepared for a flood means understanding a bit about insurance. HOMEOWNERS INSURANCE DOES NOT TYPICALLY COVER FLOODS Most important is the fact that a standard homeowners insurance policy typically doesn't cover flood damage. And because floods can occur anywhere, you should consider purchasing a separate National Flood Insurance Program (NFIP) flood policy through an insurance agent. The NFIP is managed by the Federal Emergency Management Agency (FEMA). Not everyone understands the need for a separate flood policy. In fact, research shows that there's a common misconception that homeowners insurance covers flood damage when, in fact, it typically doesn't. In a recent survey, 44 percent of Americans said they believed they were covered for weather-related floods, when, in fact, only 15 percent reported having purchased a flood insurance policy through the NFIP. HOW MUCH DOES FLOOD INSURANCE COST? Costs for flood insurance will vary depending on how much coverage you buy, what the policy covers (does it just cover the structure? the contents of your home?) and your property's flood risk. The NFIP offers flood risk maps to help you identify your community's level of risk. |

Bad News: You're Submerged. Good News? You're Also Covered...

Quick quiz: Without looking at your policy, tell us what type of water damage is covered by your homeowners or renters insurance. If you answered, “Water that comes from the top down is generally covered, but not when it comes from the bottom up,” good for you! If not, read on… Here’s something to think about: Homeowners and renters policies generally cover you for a burst pipe, or rain coming through a storm-damaged roof. But in the case of water damage caused by flooding and sewer backup, you’ll need a separate policy or endorsement. If you’re among the many homeowners and renters who don’t have flood insurance, remember this: Just because flood coverage is optional, doesn’t mean you don’t need it. Events such as 2012’s Hurricane Sandy demonstrated that you don’t have to live in a coastal region to be in danger of flooding—in fact, some of the worst flooding from Sandy occurred hundreds of miles from the nearest ocean. Another point to consider: Because flood insurance is a specialized product, available through the National Flood Insurance Program (NFIP), it has its own set of rules--deductibles, coverage limits, and so forth. Some private insurers also offer flood coverage. So what’s the best way to figure out your flood insurance needs? A good first step is to see whether your home is in an area that’s prone to flooding—you can do this by looking at FEMA.gov’s Flood Map Service Center. (FEMA also has tons of other resources to help with disaster preparation.) Another smart idea? Talk to one of our Insurance Agents. They can help you assess your risks and come up with smart insurance strategies to protect your home, family and belongings. Watch and Learn: Even a Dummy Can Be Smart about Flood Insurance! |